step one. USDA loan

Homebuyers looking to a devote an outlying town may want to use this financing. Rates of interest was aggressive, therefore do not have to place anything down. The property must be for the a qualifying region of you to sign up for a USDA mortgage.

2. FHA mortgage

FHA fund is easily offered to residents with reduced fico scores. If you make an excellent 10% deposit, you can get an FHA mortgage even although you keeps a five-hundred credit score. When you have a great 580 credit score or even more, you can get an enthusiastic FHA loan. The new FHA was a conforming loan which have constraints exactly how much you could potentially obtain regarding the financial. Men and women restrictions transform annually and you will rely on the new area’s rates from way of life.

step three. Traditional financing

Conventional funds are not covered or secured by government. Because they generally have more strict credit rating criteria, certain loan providers bring old-fashioned funds so you’re able to consumers with a credit history out-of 650. However, it can be more challenging so you’re able to safer good terms and you may appeal pricing than the consumers having highest fico scores.

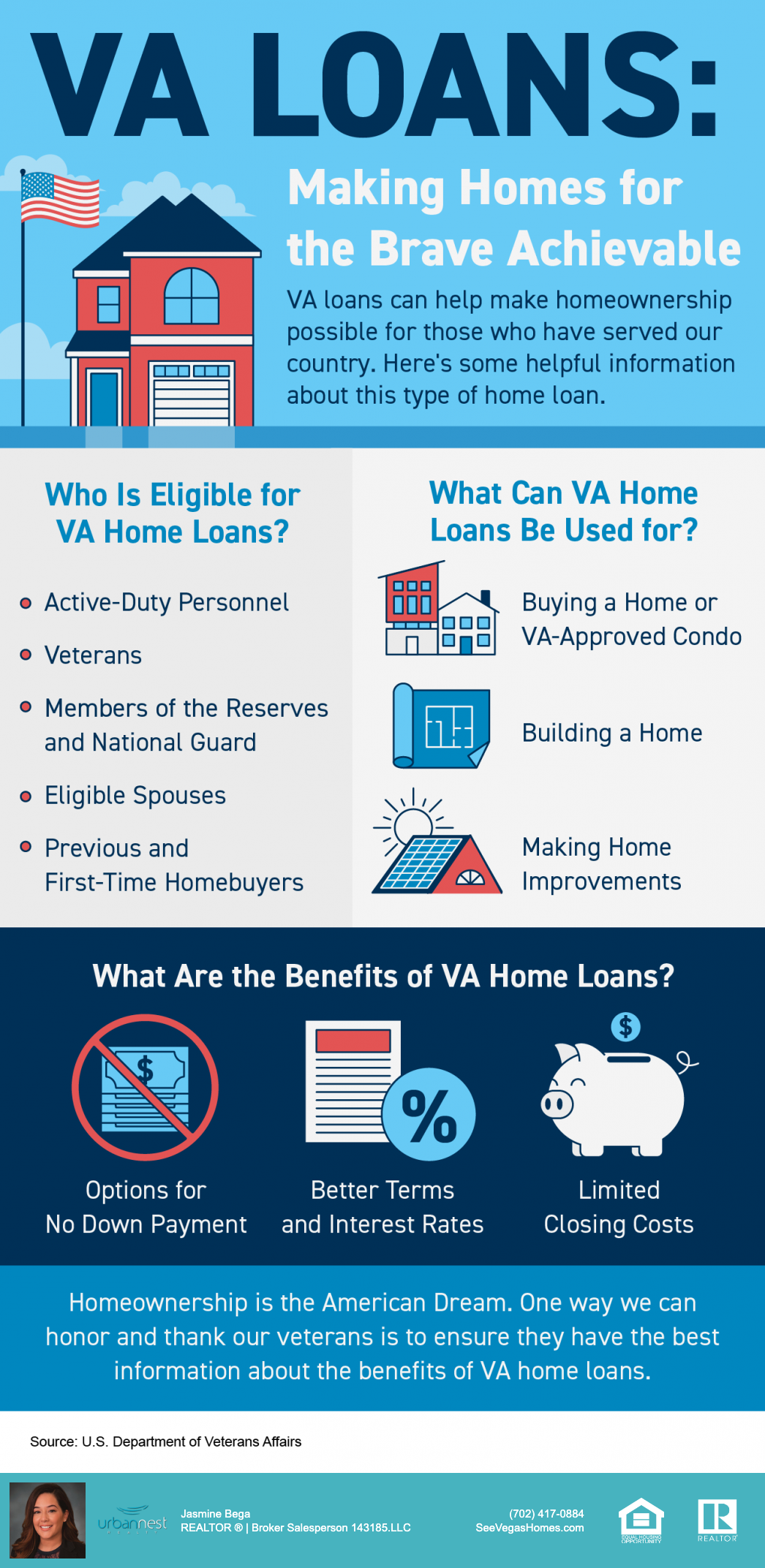

cuatro. Va financing

Virtual assistant money try exclusively for pros whom served previously otherwise is actually definitely helping. Spouses away from military members may also be eligible for Virtual assistant finance. Such money do not have down payment needs, straight down pricing, all the way down settlement costs, without personal home loan insurance.

Elevating your score can help you be eligible for higher financing amounts and help get all the way down rates. Use these techniques to replace your credit rating before you can rating nearer to buying your house.

1. Thought a card-builder mortgage

A card-builder mortgage are a secured loan who may have brief monthly premiums. The no cosigner student loans lender profile all of the fee toward borrowing agency, which will surely help alter your rating if you pay timely. Because they are secured personal loans, loan providers be big with their credit rating criteria.

When you’re doing building up your own borrowing otherwise improving your credit rating, MoneyLion has arrived to simply help! Credit Creator And (CB+)* are the effective borrowing-building subscription, and it’s built to help all of our players make or repair its borrowing, cut, expose financial literacy and tune the financial health. CB+ helps you generate otherwise improve your borrowing having accessibility a credit Builder Including loan.

A card Creator Also loan are a little loan that’s kept in the a secure account while you build monthly obligations. Since you generate payments, they are advertised on major credit reporting agencies, which will help boost your credit score with timely payments. And additionally, you have access to a few of the mortgage finance as soon because they’re acknowledged, so you’re able to utilize them for whatever you you need.

CB+ financing is an easy way to help replace your credit when you find yourself repaying your debt. Because of the enhancing your credit rating, you could qualify for all the way down rates toward future finance otherwise refinancing possibilities. And also by paying down the Borrowing from the bank Builder As well as financing on time, you could reduce your loans-to-earnings ratio, that may and alter your credit history.

2. Lower your borrowing utilization rate

Settling established loans have a tendency to alter your borrowing usage ratio, a factor that is the reason 31% of your credit score. It’s max to get your borrowing from the bank use below 10%, but delivering this ratio below 30% may also be helpful boost your rating. When you yourself have an effective $1,000 credit limit and you may are obligated to pay $100, you really have a good ten% credit use ratio.

step 3. Work at paying off financial obligation

Paying off personal debt makes your own percentage record, features a much better effect for individuals who pay everything with the time. Your own payment record makes up about 35% of your own credit history, it is therefore the biggest group. Paying down financial obligation continuously advances your own borrowing application ratio, thus concentrating on that purpose is also improve categories that affect 65% of credit rating.